Investing in Opportunity Zones allows real estate investors to defer or eliminate short-term and/or long-term gains on the sale of real property, stocks or other investments.

The federal government included an important tax incentive provision for real estate investors, developers and professionals in the federal Tax Cuts and Jobs Act that was enacted in December 2017.

This little-known section in the $1.5 trillion federal tax cut, titled Opportunity Zones, allows states across the nation to have a new tool to incentivize growth in underdeveloped, poverty-stricken areas. These incentives could become the nation’s largest economic development “program.”

The governors in each state have designated areas as “opportunity zones” from a pool of low-income census tracts and certain contiguous areas between those tracts. These areas are now eligible to use new tax incentives to attract long-term development in poor areas that lack infrastructure and jobs.

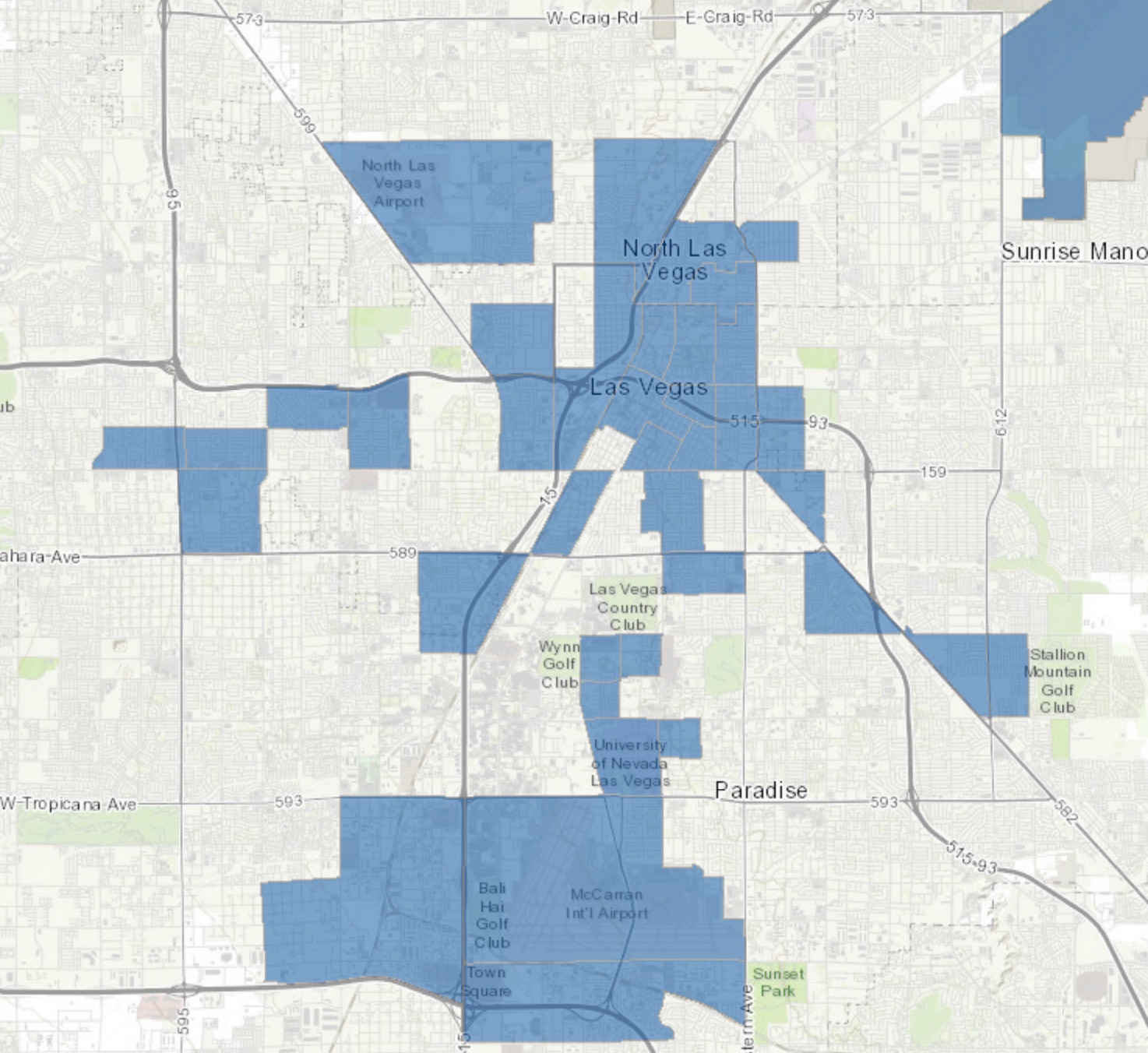

Las Vegas Opportunity Zones

Click here to see which areas are Qualified Opportunity Zones.

Of all the low-income population census tracts designated eligible for the program, governors were allowed to designate 25 percent (or at least 25 tracts in states with fewer than 100 qualified tracts) of them as Opportunity Zones. The incentive provides four tax benefits for equity investing in Opportunity Zones. Investors could take advantage of one or more of the benefits.

- Ability to Take Basis Out. Unlike a Section 1031 Tax-free Exchange transaction, when investing in an Opportunity Zone fund, the investor can choose to invest only the gain and not the full amount of the original investment. This allows the investor to take significant capital out on the sale of the original investment.

- Permanent exclusion of taxable income on new gains. For investments held in an Opportunity Fund (the investment vehicle that makes investments in Opportunity Zones) for at least 10 years, investors pay no taxes on capital gains produced through their investment. Said another way, after 10 years, the taxpayer’s basis is equal to the fair market value of the fund investment as of the date it is sold or exchanged.

- Basis step-up of capital gains invested. For capital gains placed in Opportunity Funds for at least five years, investors’ basis on the original investment is increased 10 percent. If invested for at least seven years, investors’ basis on the original investment is increased 15 percent, thus reducing the tax liability by 15 percent.

- Temporary deferral of taxes on capital gains. Investors can place existing assets with accumulated capital gains into Opportunity Funds. Those capital gains are not taxed until the end of 2026 or when the asset is disposed of.

Except for the exclusion of a few “sin” businesses, the activities and projects Opportunity Funds can finance are broad. Opportunity Funds can finance commercial and industrial real estate, multifamily properties, housing, infrastructure, and current or start-up businesses. At least 90 percent of an Opportunity Fund must be invested in a qualified Opportunity Zone.

For real estate projects to qualify for Opportunity Fund financing, the investment must result in the properties being “substantially improved,” such as upgrading existing properties or building on available land in a zone.

Potential for Tax-Free Treatment of Future Real Estate Appreciation

If an investment of existing capital gains is held for 10 or more years in an Opportunity Fund and eligible Opportunity Fund investments, at disposition or sale of the Opportunity Fund interest, the appreciation on the initial investment would not be subject to taxation.

For example, if a multifamily developer would invest $20 million in an Opportunity Fund that invests in eligible qualified Opportunity Zone property (i.e. new apartments in the zone and other commercial properties) and the investment appreciates to $35 million over a 10-year investment horizon, the $15 million of capital gain would be tax-free to the investor at disposition or sale of the interest in the Opportunity Fund.

This tax-advantaged treatment of long-term investments in qualified Opportunity Zones provides significant planning opportunities for real estate, project finance, and infrastructure projects.

Investors will benefit most in Opportunity Zone financing when the underlying assets, real property or business investments are subject to rapid 10-year appreciation. Because of this, utilization of Opportunity Zone financing with structured leveraged may result in substantial tax-advantaged appreciation vis-à-vis traditional real estate investment models.